fin-3610 · Risk and return

Estimating the Cost of Capital

Practical recipes for estimating the cost of equity (via CAPM with realistic inputs), the after-tax cost of debt, and how to choose project-specific vs firm-wide discount rates.

Learning objectives

- Estimate cost of equity from CAPM with realistic input choices.

- Estimate the pre-tax and after-tax cost of debt from current market yields.

- Assemble the WACC from the cost of equity and after-tax cost of debt at given capital-structure weights.

- Adjust for project-specific risk vs firm-wide risk in capital budgeting.

Three discount rates that get confused

When valuing things you’ll use one of three discount rates:

- Cost of equity — the rate equity holders demand.

- Cost of debt — the rate debt holders demand. (Pre-tax and after-tax versions matter.)

- WACC — weighted average of the two, used to discount FCF.

Different cash flows need different rates. FCFE → . Project free cash flow → WACC. Pre-tax operating cash flow → also WACC, but conceptually. Get the rate-cash-flow matching wrong and your valuation is meaningless.

This lesson estimates and in practice and assembles them into the WACC. How a firm’s choice of capital structure changes the WACC, and whether an optimal debt mix exists, is the subject of Unit 5; here we take the weights as given and compute the rate.

Cost of equity from CAPM

We saw the formula:

Now the practical input choices:

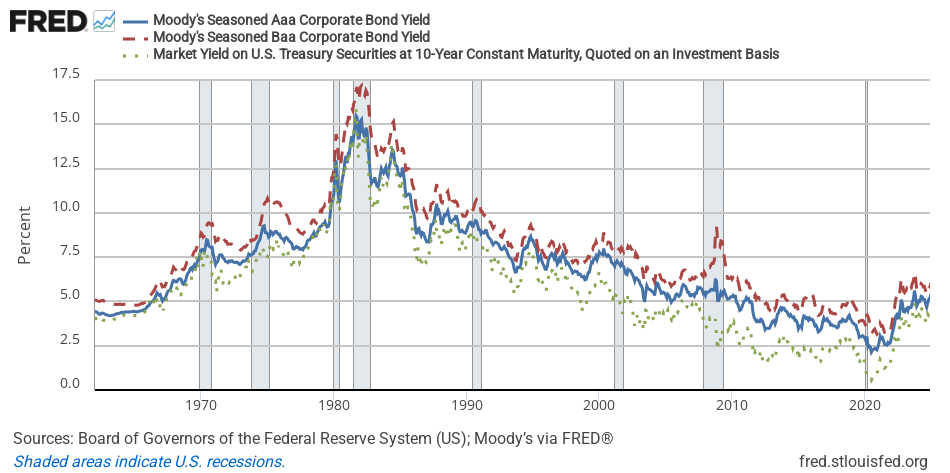

Pick matching the horizon. A 5-year project: 5-year Treasury yield. A 10-year DCF: 10-year. A perpetual valuation: long- end of the curve (10-30 year average). Don’t use the federal funds rate or 3-month T-bill for long-horizon DCFs — the term premium is real and you need to include it.

Pick a defensible market risk premium. Three common approaches:

- Historical: long-run average of stock returns minus T-bill. ~5-7% for US.

- Implied: solve a multi-stage DDM with current S&P 500 price and consensus earnings/dividends for the discount rate that makes them consistent. Tends to give 4-6%.

- Survey: ask CFOs or finance professionals. CFO surveys (Duke) typically yield 5-6%.

Most finance practitioners settle on 5-6% as a working assumption. Don’t pick 8%+ unless you can defend it specifically.

Pick beta carefully. Use 60 monthly observations against a broad market index. Smooth out single-observation outliers (some providers Winsorize). For sectors with small samples or thin trading, use industry-average beta from comparable public firms rather than firm-specific noise.

For a private firm, the public-comparable approach is standard:

- Find 5-10 public comparables.

- Look up each one’s levered beta.

- Unlever each one (remove the leverage effect): .

- Average the unlevered betas.

- Re-lever at your target’s capital structure: .

- Plug into CAPM.

The unlever/re-lever procedure isolates business risk from financial-structure risk, so you’re comparing apples to apples.

Cost of debt

Two ways to estimate:

1. Market YTM on existing debt. If the firm has publicly traded bonds, take the YTM of those bonds (matched to the planned horizon). That’s the rate the market currently demands for the firm’s credit risk.

2. Synthetic rating + spread table. If the firm doesn’t have public debt, estimate what rating it would get based on coverage ratios and leverage, then add the typical spread for that rating to the Treasury benchmark. Damodaran (NYU Stern) publishes a synthetic- rating table widely used in practice.

Don’t use the coupon rate on legacy debt — that’s a historical artifact, not the market’s current view. If a firm issued a 3% bond in 2020 but trades at 6% YTM today, 6% is what new debt would cost.

Pre-tax vs after-tax. The after-tax cost of debt is

Interest is tax-deductible, so the firm’s true cost of debt is reduced by the tax shield. WACC always uses the after-tax rate.

Project risk vs firm risk

If you’re using the firm’s WACC to discount a project, you’re implicitly assuming the project has the same risk as the average of the firm’s existing assets. This is right for projects that look like the firm’s main business. It’s wrong when:

- The project is in a much riskier (or safer) business than the firm’s main activity. A consumer-staples firm building a biotech R&D division shouldn’t use its low cost of capital for that project — biotech is much riskier.

- The project has a fundamentally different capital structure than the firm.

The fix: use the division-specific or project-specific cost of capital. Start with the unlevered beta of pure-play comparables in that business, re-lever at the project’s planned capital structure, plug into CAPM.

This is one of the most common mistakes in real-world capital budgeting. A firm with low WACC easily over-invests in risky new ventures because the discount rate they’re applying is too low for the actual risk.

A worked example

Estimate cost of capital for a hypothetical mid-cap industrial manufacturer.

Cost of equity:

- = 4.2% (10-year Treasury).

- MRP = 5.5%.

- Beta = 1.1 (from FactSet, 60-month regression).

- .

Cost of debt:

- Existing 10-year bonds trade at 6.0% YTM.

- Tax rate 25%.

- .

Assembling the WACC. Weight each rate by its share of the firm’s value , and use the after-tax cost of debt:

Say the firm is financed $700M equity and $300M debt, so and :

That 8.53% is the discount rate for the firm’s free cash flow. Each input is also useful on its own: for FCFE-based valuations, for bond-portfolio pricing.

The weights here are taken as given. Whether the firm could lower its WACC by changing the mix, and what stops it from using all debt, is the capital-structure question of Unit 5.

What’s hard

The single biggest source of error in cost-of-capital estimation is not the formulas — they’re trivial — but the input choices. Sensitivity-test every estimate. If your DCF says $50 per share at 10% WACC and $30 per share at 11%, the dispersion in plausible WACC estimates is meaningful. Present a range, not a point.