eco-1002 · Money and monetary policy

The Fed's Balance Sheet and the Money Supply

How the Federal Reserve's assets and liabilities determine the monetary base, and how that base is multiplied into the broader money supply through bank lending.

Learning objectives

- Explain the relationship between the Fed's balance sheet and the monetary base.

- Derive the equation for the simple deposit multiplier and use T-accounts to illustrate multiple deposit creation.

- Explain how the actions of banks and the nonbank public affect the money multiplier.

The Fed’s balance sheet

The Federal Reserve, like any bank, has a balance sheet. Its assets are primarily Treasury securities and (since 2008) mortgage-backed securities. Its liabilities are currency in circulation and bank reserves. Together those two liabilities form the monetary base, often denoted or :

When the Fed buys \1$1$1$B. This is the central fact that makes the Fed’s open-market operations a monetary-policy tool.

From base to broad money

The monetary base is small. The actual money supply (M1, M2) is much larger because banks lend out a fraction of every deposit, and those loans become new deposits at other banks. The ratio between and is the money multiplier :

In the simple case where banks hold a fraction of every deposit as reserves and the public holds no currency, repeated re-lending gives the simple deposit multiplier . With , \1$10$ of deposits.

The realistic money multiplier

Two leakages shrink the multiplier:

- The public chooses to hold some currency. Let be the currency-deposit ratio.

- Banks hold some reserves beyond what’s required (excess reserves). Let be the total reserve-deposit ratio.

The full money multiplier is

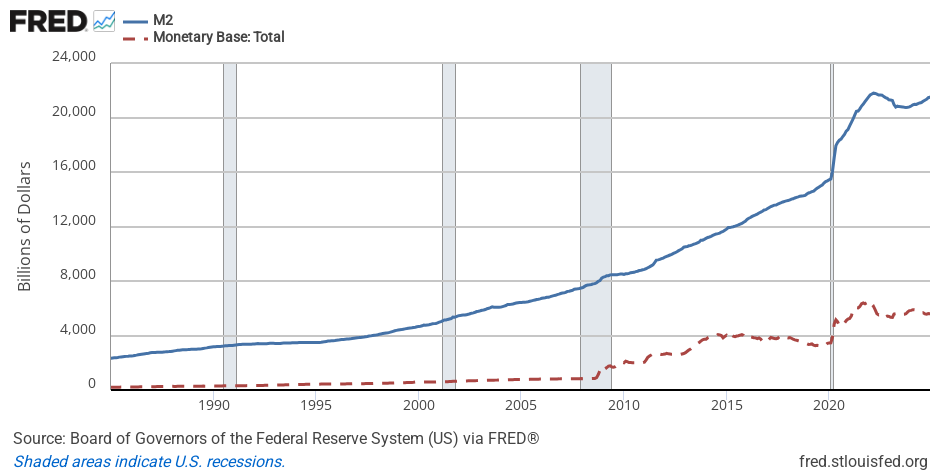

Both leakages reduce . After 2008, rose dramatically because the Fed began paying interest on reserves and banks chose to park excess reserves there instead of lending. The multiplier fell, so even though the Fed expanded enormously (quantitative easing), rose much less than did.

Play with it

Money supply M = m · MB where m = (1 + C/D) / ((C/D) + (R/D)). As banks hold more excess reserves (R/D ↑) or the public holds more cash (C/D ↑), the multiplier shrinks. This is why QE's effect on M depends on what banks do with the new reserves.

Try raising from 0.10 to 0.30. Notice that the multiplier roughly halves — that’s the QE-era story in one chart.

Where the policy lever is

The Fed directly controls (through open-market operations, discount lending, and the size of its balance sheet). It influences indirectly through the interest rate it pays on reserves. It does not control — that’s a household choice driven by trust in banks and the cost of holding cash. This division of control is why monetary policy transmission can be slow and uncertain.