eco-1002 · Money and monetary policy

Monetary Policy Tools and Targets

The Federal Reserve's goals, the policy tools it uses to influence the federal funds rate, and how monetary targeting fits into the broader policy framework.

Learning objectives

- Describe the goals of monetary policy.

- Understand how the Fed uses monetary policy tools to influence the federal funds rate.

- Explain the role of monetary targeting in monetary policy.

The goals of monetary policy

The Federal Reserve operates under a dual mandate set by Congress in the Federal Reserve Reform Act of 1977: pursue maximum employment and stable prices. In practice the Fed names several supporting goals:

- Price stability — typically a 2% inflation target on PCE.

- High employment — operationally, unemployment near its natural rate.

- Stability of financial markets and institutions — orderly liquidity provision.

- Economic growth — sustainable real output growth.

- Interest-rate stability — avoiding sudden, large rate swings.

- Foreign-exchange market stability — avoiding disorderly currency moves.

These can pull in different directions. A central debate of the 2022-2026 inflation episode was how to bring inflation down without forcing a sharp rise in unemployment.

The tools

The Fed has three primary tools and one newer one:

- Open-market operations. The Fed buys or sells Treasuries (and now MBS) on the secondary market, swapping reserves for securities. Buying expands reserves and the monetary base; selling contracts both. This is the day-to-day lever.

- Discount-window lending. The Fed lends directly to banks at the discount rate. Used heavily in crises (2008, 2020) but a small share of Fed activity in normal times.

- Reserve requirements. Historically the Fed set the fraction of deposits banks had to hold as reserves. The Fed cut required reserves to zero in March 2020 and has not restored them.

- Interest on reserves (IORB). Since 2008 the Fed pays interest on reserves held at the Fed. By raising IORB the Fed creates a floor under short-term rates without having to drain reserves through open-market sales — a key tool in the post-QE era.

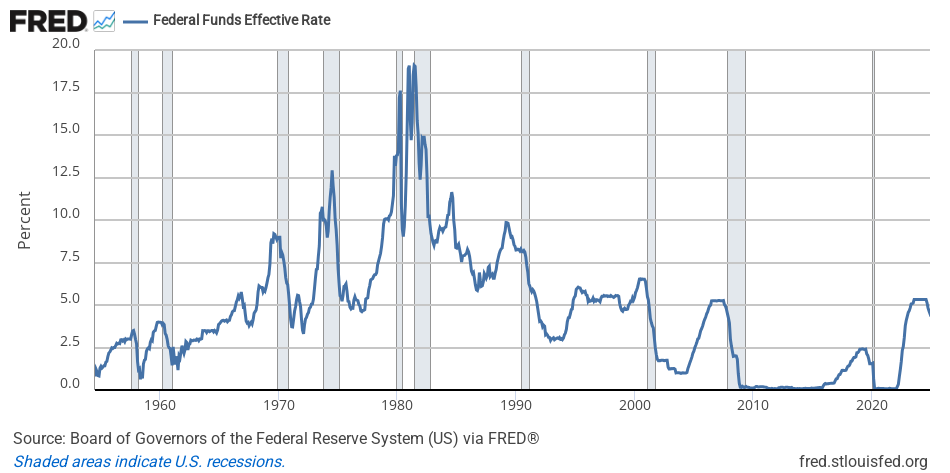

The federal funds rate as a target

Banks borrow reserves overnight from each other at the federal funds rate (FFR). The Fed targets this rate as its primary policy variable. Open-market operations and IORB are the tools; the FFR is the target.

Transmission to the broader economy:

- FFR ↑ ⇒ short-term rates ↑ ⇒ longer-term rates ↑ (with a lag) ⇒ borrowing cost ↑ ⇒ consumption + investment ↓ ⇒ aggregate demand ↓.

- FFR ↓ runs the chain in reverse.

The chain has long and variable lags (Friedman’s phrase). Empirically, peak effects on output show up 12-18 months after a rate change; peak effects on inflation, 18-24 months out.

Monetary targeting vs interest-rate targeting

In the 1970s and early 1980s, under Paul Volcker, the Fed briefly targeted money-supply growth directly (M1 / M2 targets). That regime ended because the velocity of money became unstable as financial innovation made the relationship between and nominal GDP unreliable.

Since the mid-1980s the Fed has targeted the FFR. Money-supply data is still published and watched, but the policy lever is the interest rate.

Reading the FOMC statement

Eight times a year the Federal Open Market Committee announces a target range for the FFR (currently in 25-basis-point bands). The accompanying statement signals the Fed’s read of the economy and its bias for the next meeting. The market reaction is usually larger than the rate change itself, because future rate expectations move with the statement’s forward guidance.